Trying to find a cosigner for an apartment can be an uncomfortable situation on the surface. But being asked for a cosigner by a landlord is more common than you think, and it can increase your chances of getting approved. Understanding what it means, for you and for whoever you plan to sign with, makes the whole process easier to navigate.

Here’s what you need to know before any signatures happen.

What Is a Cosigner for an Apartment?

A cosigner is someone who signs the lease with you and agrees to be financially responsible if you can’t pay. It’s often a parent, sometimes a sibling, or a close friend. It’s most common for newly established adults who don’t have a credit score or history of renting, but it can also extend beyond these circumstances.

A cosigner doesn’t usually live in the unit—they have no key, no right of access, and no say in what happens inside the apartment. What they do have is full financial liability. If you miss rent in March, your landlord can go straight to your cosigner for the full amount of March’s rent. The legal term for this is “jointly and severally liable,” which sounds technical but really just means the landlord can choose whom to pursue, and they’ll choose whoever’s easier.

So what is a cosigner for an apartment, really? Someone who trusts you enough to tie their financial reputation to your ability to pay rent on time. That’s the actual ask.

When Landlords Require a Cosigner

A few situations come up constantly.

- No credit history, or a thin one. This catches many first-time renters off guard. Students, people who’ve never had a credit card, recent arrivals to the US who haven’t had time to build a US credit profile – none of that means anything is wrong, but from a landlord’s perspective, there’s nothing to evaluate. A cosigner fills the gap.

- Income under the rental rate threshold. Most landlords want to see 2.5 to 3x monthly rent in verifiable income. If you’re not there yet, a cosigner with a stronger financial picture can bridge that.

- Prior eviction or recent financial trouble. It’s not automatically disqualifying everywhere, but it can be seen as a risk to a landlord. A cosigner is often what makes the deal work.

- Cosigner policies that apply regardless of individual circumstances. International students are a common example, because income verification across borders is complicated, and landlords take the path of least resistance.

Pro Tip: If you’re not approved due to your credit score, our guide on renting with bad credit has more tips.

How Cosigning a Lease Works

It’s more involved than most people expect going in. The cosigner doesn’t just sign at the end – they go through their own screening. It may include:

- Credit check

- Income verification

- Sometimes employment confirmation

Landlords treat them essentially as a second primary applicant, because that’s what they are.

Both names go on the lease. Liability starts day one, not when something goes wrong. And here’s the thing that regularly catches cosigners off guard: if the lease auto-renews and the cosigner clause doesn’t have an explicit expiration, that obligation rolls forward into the renewal too. A cosigner who thought they were on the hook for twelve months can end up being on the hook for much longer.

Be sure to read the cosigner clause before anyone signs anything. If you’re the one being asked to cosign, this deserves the same attention you’d give a lease on your own place – because in financial terms, that’s effectively what it is.

Cosigner vs. Guarantor: What’s the Difference?

Technically, there is a slight difference, though landlords and renters use the terms interchangeably enough that the distinction gets blurry.

- A cosigner signs the actual lease. Liability starts immediately, alongside the tenant.

- A guarantor signs a separate guaranty agreement and is only called on if the tenant actually defaults – they’re not a party to the lease itself, more of a backup that activates under specific conditions.

Financial exposure is similar either way. The difference is timing and which document triggers the obligation. If a landlord asks for either one, ask exactly what they want signed and when liability kicks in. Don’t assume the terms mean the same thing to them as they do to you.

What Does It Mean to Cosign for an Apartment?

What does it mean to cosign? In plain terms, you’re agreeing in writing to pay someone else’s rent if they don’t.

That includes unpaid rent, late fees, and damage costs that exceed the security deposit. If the tenant’s account goes to collections, you’re named. If the landlord takes legal action, you’re a party to it. Your credit report can take hits from the tenant’s missed payments, even though you never lived there, never caused the damage, and never chose to stop paying.

How to Find a Cosigner

Start with family, if that’s an option. Parents are the most common cosigners, followed by siblings and close family friends. As long as the relationship is one you trust and feel supported by, it matters less how the cosigner is related (or not).

Financial and Other Requirements

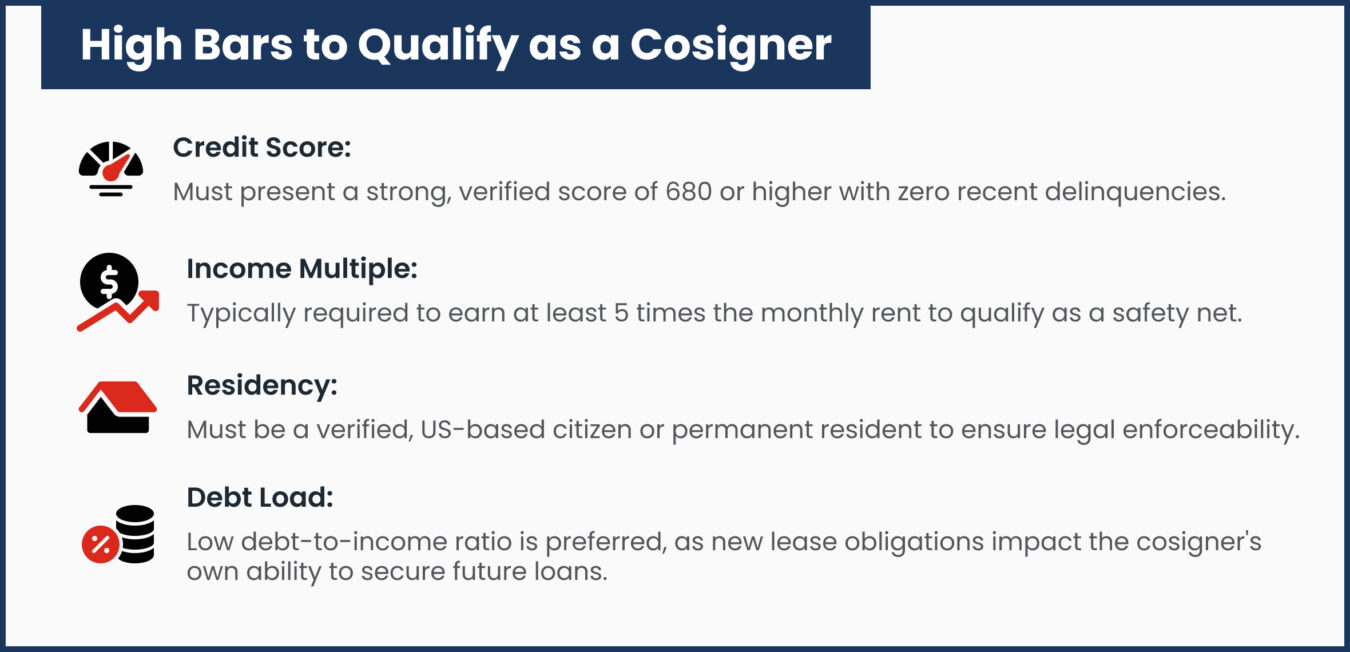

Most landlords prefer cosigners who are US residents with credit scores of 680 or higher and income at least 5 times the monthly rent. For a $1,200/month apartment, that’s about $6,000 in income. It rules out people with modest incomes, even if their credit is fine, so confirm the landlord’s exact criteria before you approach someone.

When you have that conversation, don’t soften the details. Explain the full lease term, the liability, and your plan for making sure they never have to actually cover anything. Our guide on what to expect during the rental application process lays out landlord requirements in more detail, which can help you prepare ahead of time.

Pro Tip: If you’re in a situation with no credit at all, the guide to renting with no credit has some alternatives worth knowing about, too.

Cosigner Services: A Paid Alternative

Not everyone has someone to cosign with. In this case, there are companies that can act as a cosigner or guarantor for an additional fee. There are a few caveats:

- Not every landlord accepts third-party services, so confirm acceptance before you pay anything.

- If you go this route, get quotes from more than one service, since pricing isn’t standardized and varies more than you’d expect.

Risks for the Cosigner

The risks of being a cosigner aren’t hypothetical. If the tenant pays late, it can appear on your credit report. Additionally, the lease obligation factors into your debt-to-income ratio, which affects your ability to borrow during the entire lease term.

Signing for someone with a history of financial instability is a different calculation than signing for someone who has had one rough patch and is on steadier ground. The relationship matters, but it doesn’t eliminate the financial exposure.

Before you sign anything:

- Read the entire lease, not just a few clauses

- Ask specifically whether the obligation carries through on renewal

- Think about putting a simple informal side agreement in writing with the tenant – not a legal document, just a mutual understanding that they’ll tell you immediately if a payment is in jeopardy

How to Get Released from a Cosigner Obligation

If you’re a cosigner and would like to get released, this is where things get complicated. A cosigner is typically on the hook until the lease or loan ends.

In the case of an apartment rental, a lease renewal is one option. If the tenant’s credit and income have improved enough to qualify independently, they can apply for the renewal without the cosigner. Some landlords will agree to a mid-lease release after 6 or 12 months of on-time payments.

But here’s what won’t do it: subletting, adding a roommate, or any informal transfers.

If you’re cosigning and looking for a way out, lease renewals or term ends are your best bet. So choose wisely!

Tips for Both Tenants and Cosigners

Here are our best tips for tenants looking to have a cosigner for the first time:

- Set up autopay. Don’t wait – do it before your first month of rent is due.

- Communicate with your cosigner every month when rent posts.

- If a problem is coming, tell your cosigner ahead of time.

If you’re a cosigner for an apartment, here’s what you need to know:

- Read the lease before signing so you understand the late payment terms and how they work.

- Find out how long the lease is for and how long you are acting as a cosigner. (Usually the end of the lease term.)

- Get the landlord’s contact information and know how to reach them directly if needed.

Need to find an apartment? Browse through Rentler’s large network of rentals near you, completely free.

Frequently Asked Questions About Apartment Cosigners

What is a cosigner for an apartment?

Å cosigner is someone who signs a loan or lease alongside the primary person and agrees to cover the financial damages if the primary person cannot. It is usually used when the primary person or potential tenant has a negative or insufficient credit history.

Can anyone be a cosigner?

Landlords typically require cosigners who have a US residency, a credit score of 680, and income of at least five times the monthly rent. Check the landlord’s specific requirements before you ask anyone.

Does cosigning hurt my credit?

The act of cosigning does not hurt your credit, but the outcomes of who you cosign with can. If the tenant you cosign with pays rent late, it will show up on your credit card. If their account goes to collections, you’ll be financially responsible. The lease obligation also shows up in your debt-to-income ratio.

How long is a cosigner responsible?

A cosigner is responsible for the full lease or loan term. If the lease auto-renews and the cosigner clause doesn’t have an explicit end date, the obligation extends into the renewal. A written release from the landlord or a lease update without the cosigner is the only thing that can remove a cosigner.

What’s the difference between a cosigner and a co-applicant?

In terms of a rental application, a co-applicant is someone who plans to live in the unit, while a cosigner is a financially liable person who typically doesn’t live in the rental with the cosignee. Same financial liability in terms of the landlord being able to pursue them, but completely different living arrangements.

Can I cosign if I have a mortgage?

Yes, if the mortgage lenders allow it. You’ll need to check with your loan provider or realtor to know your individual limits.