TL;DR:

A guarantor is a third party who legally agrees to cover rent if the tenant cannot pay—without living in the unit or signing the lease itself. Landlords typically require one when a renter has limited credit, low income relative to rent, or no established rental history, and guarantors usually need a credit score of 700+ and income of 80 times the monthly rent. Paid guarantor services are available for renters without a personal option, charging roughly 60% to 100% of one month’s rent as a non-refundable fee.

What Is a Guarantor for an Apartment? A Renter’s Guide

Apartment applications come with a long checklist—proof of income, credit checks, references—and for many renters, a guarantor is one more requirement on that list. If a landlord has asked for one during the rental application process, the request might feel intimidating, but it shouldn’t be. A guarantor is simply a third party who agrees to cover rent if the tenant cannot pay.

Knowing what is a guarantor for an apartment and why landlords request one puts renters in a much stronger position. This guide covers when you might need a guarantor, how the role differs from a cosigner, what qualifications are involved, and what to watch for in the paperwork.

Guarantor Definition

A guarantor is a third party who legally agrees to pay rent or cover damages if the tenant fails to do so, without being a party to the lease itself. In most cases, this person signs a separate guaranty agreement rather than the lease directly.

The term comes up most often in NYC and other competitive rental markets. Renters who find themselves asking “what is a guarantor for an apartment” are usually right in the middle of an application and want a clear answer. In other parts of the US, people tend to say “cosigner,” though the two roles carry technical differences worth understanding.

So what is a guarantor for a lease in practical terms? Someone who gives a landlord financial reassurance—a safety net that can make the difference between an approved application and a denied one. The rest of this guide breaks down when that safety net is needed, how it works, and what both sides should consider before signing.

When Apartments Require a Guarantor

A landlord asking for a guarantor does not mean they dislike your application. It usually means they want an extra layer of financial protection before approving the lease. Understanding the most common reasons can help renters prepare early:

- Low income compared to rent: In NYC, renters are often expected to earn 40 times the monthly rent. In many other markets, landlords look for income equal to 2.5 to 3 times the monthly rent.

- Limited or no credit history: First-time renters and anyone renting with bad credit may face a closer review during screening.

- Student status or international renter: Renters without an established US rental history may be asked to provide extra financial backing.

- Recent job change or self-employment: If your income is harder to document, a landlord may ask for added security before approving the application.

Some buildings apply blanket guarantor requirements for any applicant under a specific income threshold. Competitive luxury rentals, in particular, often default to requiring a guarantor for younger applicants who may not yet have a long earnings history. None of this means the application is dead on arrival—it just means the landlord wants additional assurance that rent will be paid.

Renters often see “guarantor” and “cosigner” used interchangeably during the apartment search. The two terms are related, but they are not identical.

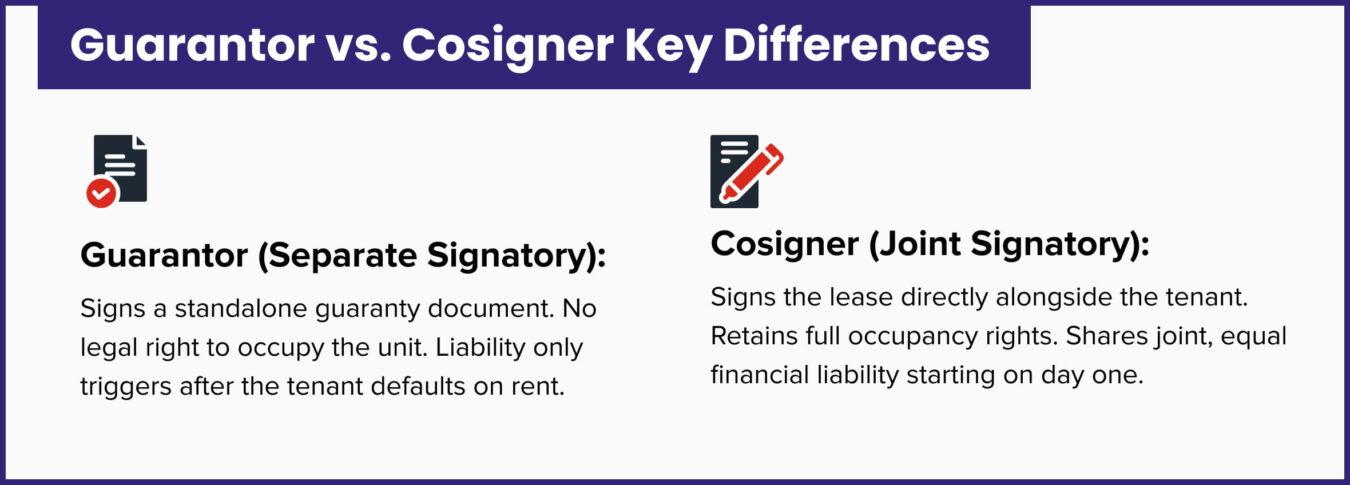

Guarantor vs. Cosigner: Are They the Same?

In everyday conversation, the two terms are frequently swapped without a second thought. Technically, though, there is a clear difference between them.

A guarantor signs a separate guaranty document—not the lease—and becomes liable only if the tenant defaults on payment. A guarantor does not have the right to live in the unit. A cosigner, on the other hand, signs the lease itself and shares joint legal responsibility from day one. Cosigners may or may not live in the apartment, but their financial obligations begin the moment ink hits paper.

The practical outcome is similar, since both parties are on the financial hook if the tenant cannot pay. Regional language varies, too. NYC overwhelmingly uses “guarantor,” while California and many Western markets lean toward “cosigner.” The distinction matters most when reading the actual documents, so renters should pay close attention to what they—and their support person—are being asked to sign.

Regardless of the label, it helps to understand the specific obligations a guarantor takes on once the agreement is in place.

What Does a Guarantor Do?

The primary obligation is straightforward: pay rent if the tenant fails to do so. Under most guaranty agreements, landlords can pursue the guarantor directly once a payment is missed—no waiting period or separate notification is required.

A guarantor may also be responsible for more than unpaid rent. If the tenant damages the apartment and the security deposit does not cover the full repair cost, the guarantor may have to pay the remaining balance. If neither the tenant nor the guarantor pays what is owed, the landlord may take legal action against both of them.

That said, a guarantor is not a roommate or backup tenant. They do not have the right to enter, use, or live in the apartment. Their role is financial only. It is also important to check how long it lasts. Some agreements end with the original lease term, while others continue automatically when the lease renews. Renters and guarantors should read the full agreement carefully before signing.

Given these responsibilities, landlords set a high bar for who qualifies as a guarantor in the first place.

Guarantor Qualifications

Before asking someone to act as a guarantor for an apartment, renters should understand the qualification standards most landlords apply. The requirements are stricter than what tenants themselves need to meet:

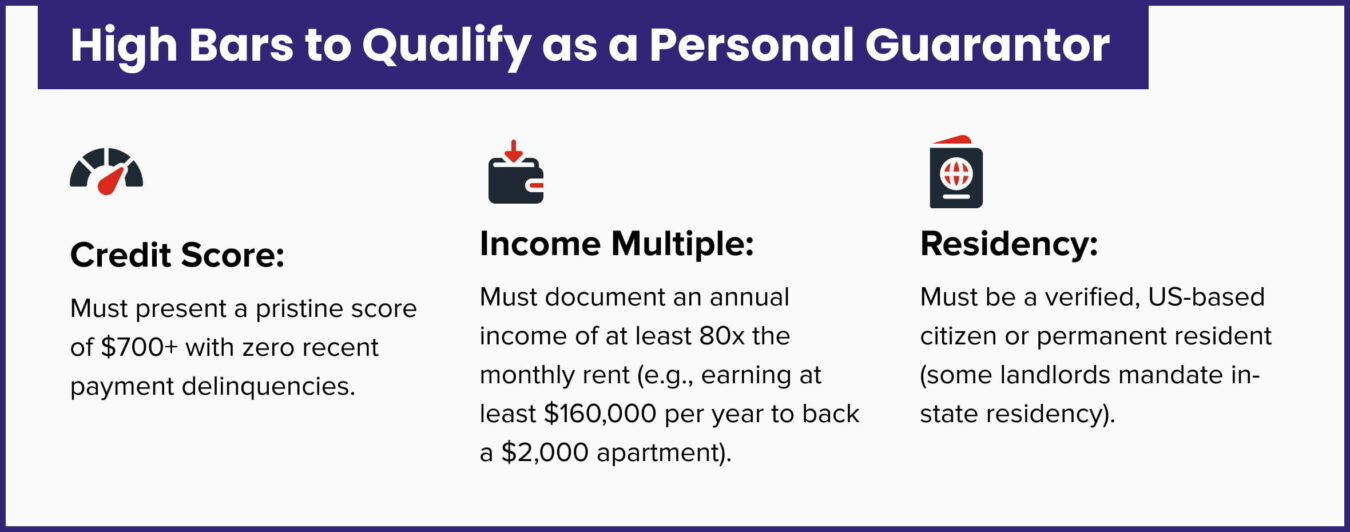

- US-based residency: Most landlords accept out-of-state guarantors, but it is rare to accept someone based outside the country.

- Strong credit score: A score of 700 or above is the typical minimum, though some buildings set the bar even higher.

- High income: The standard in NYC is 80 times the monthly rent. In other markets, the range is 40 to 80 times. For a $2,000-per-month apartment, that means the guarantor needs to earn at least $160,000 per year.

- No major debt issues: Derogatory credit marks, active collections, or high debt-to-income ratios can disqualify a candidate.

Landlords often want more than a few recent pay stubs. Many ask for tax returns to confirm the guarantor’s income, and some buildings may even require the guarantor to own property in the same state. It is worth checking these details before asking someone to complete paperwork.

The process is similar to getting an apartment with no credit: preparation matters. Ask the landlord for their exact requirements upfront so your guarantor knows what to expect.

Once the qualifications are clear, the next step is figuring out who to ask.

How to Find a Guarantor

The most common choice is a parent, and for good reason. Parents tend to have the established income, credit history, and willingness to help that the role demands. Siblings, other relatives, and longtime close friends with strong finances are also solid options.

That said, the income requirement narrows the pool considerably. For a $2,500-per-month apartment, a guarantor in NYC would need to earn roughly $200,000 per year. That is a high bar, and not everyone has a family member who meets it.

Renters should approach the conversation with full transparency—share the lease terms, your own financial picture, and your plan for making rent payments on time. The guarantor is taking on real financial risk, so honesty matters. This kind of candor is especially important for anyone apartment hunting while unemployed and relying on a support person to strengthen the application.

When a personal guarantor is not an option, paid services offer an alternative.

Guarantor Services: The Paid Alternative

Not every renter has a high-earning family member or friend willing to sign a legal document on their behalf. For those situations, third-party companies can step in as a guarantor for an apartment application in exchange for a fee.

The idea is fairly straightforward. A guarantor company takes on the financial risk for a one-time fee, usually equal to 60% to 100% of one month’s rent. Services such as The Guarantors and Insurent work with landlords in many major rental markets to help renters get approved.

The downside is the cost. Renters may avoid an awkward conversation with a parent, relative, or friend, but the fee is usually non-refundable. For a $3,000-per-month apartment, that could mean paying $1,800 to $3,000 upfront. It is smart to compare quotes from more than one service and include this expense when budgeting for other rental application fees.

Whether relying on a personal guarantor or a paid service, the guaranty agreement itself deserves careful attention.

The Guaranty Agreement: What to Read Carefully

Finding the answer to the question “what is a guarantor for an apartment” is only half the equation. The guaranty agreement is where the specific obligations live, and anyone acting as a guarantor for a lease should read it with the same scrutiny they would give their own housing contract.

Key clauses to review:

- Liability scope: Does the agreement cover rent only, or does it extend to damages, late fees, and legal costs?

- Duration: Is the commitment limited to the initial lease term, or does it carry over through renewals?

- Termination conditions: How and when can the guarantor be released from the obligation?

- Jurisdiction: Where would any legal dispute be handled?

Some agreements include joint and several liability, which means the landlord can pursue the guarantor before or instead of pursuing the tenant for missed payments. That is a significant detail to catch before signing. Guarantors should keep a signed copy of the agreement and store it alongside any documentation from applying for a property online, so records are complete and accessible.

Understanding the fine print is important, but guarantors should also take a realistic look at the financial risks they are accepting.

Risks for the Guarantor

What is a guarantor according to the guarantor’s side? Consider the potential downsides carefully. Taking on someone else’s housing debt is a serious commitment, and the consequences of a tenant default are real.

If the tenant falls behind and the guarantor cannot pay the balance, the consequences can become serious. Missed payments or collection accounts may show up on the guarantor’s credit report and hurt their score. The landlord may also sue to recover the unpaid rent, which can add attorney fees and court costs.

There is another risk that is easy to overlook. Taking on a guaranty may affect the guarantor’s debt-to-income ratio, which could make it harder for them to qualify for a mortgage or another loan. Before signing, both the renter and guarantor should be honest about whether the arrangement is financially realistic.

To stay ahead of problems, guarantors should set up a system for monthly rent confirmation. Asking the tenant to share auto-pay receipts or payment confirmations each month prevents surprises. A short written side agreement between the tenant and guarantor—covering communication expectations and a plan if the tenant’s financial circumstances change—adds a helpful layer of protection.

Given these risks, it is natural for guarantors to ask how and when they can walk away from the obligation.

How to Release a Guarantor from the Obligation

The easiest path to releasing a guarantor for a lease is at renewal time. If the tenant has improved their income or credit score during the initial term, they can reapply without a guarantor and sign a new contract independently.

Some landlords will also agree to release a guarantor after 12 or more months of on-time payments, particularly if the tenant’s financial profile has strengthened. Outside of that, the obligation typically concludes when the lease term ends—provided the agreement does not auto-renew.

This is an important point to catch before signing. Some guaranty agreements renew automatically with the lease. That means the guarantor may remain responsible unless the landlord releases them in writing. Renters can try to negotiate an early-release clause at the start, such as allowing the guarantor to exit after a certain number of on-time rent payments.

Subletting does not automatically remove the guarantor either. Unless the landlord formally changes the lease and guaranty agreement, the original guarantor may still be responsible.

Frequently Asked Questions

What is a guarantor for a lease?

A guarantor for a lease is a third party who agrees to cover rent and potentially other costs if the tenant cannot pay. This person signs a separate guaranty agreement—not the lease itself—and becomes legally responsible for the tenant’s financial obligations for the duration of the contract.

How much does a guarantor service cost?

Most guarantor services charge a one-time, non-refundable fee between 60% and 100% of one month’s rent. The exact amount depends on the renter’s credit profile, income, and local market conditions. Rates tend to be higher for applicants without US credit history. Comparing quotes from multiple providers is recommended.

Can a guarantor live in another state?

Yes, many landlords accept out-of-state guarantors, though policies vary by property. In NYC, some landlords prefer guarantors who reside within New York State, but it is increasingly common to accept someone from anywhere in the US. Always confirm the landlord’s specific policy before applying.

Does being a guarantor affect my credit?

Signing a guaranty agreement does not directly impact a guarantor’s credit score. However, if the tenant defaults and the guarantor cannot cover the unpaid amount, missed payments or collection accounts can appear on the guarantor’s credit report and lower their score over time.

How long is a guarantor responsible?

A guarantor is typically responsible for the full term of the lease. Some agreements extend through renewals unless the guarantor is explicitly released in writing. The duration should be clearly stated in the guaranty agreement, and both the tenant and guarantor should review this clause carefully before signing.

What’s the difference between a guarantor and a cosigner?

A guarantor signs a separate agreement and becomes responsible only if the tenant defaults on rent. A cosigner signs the lease itself and shares equal financial responsibility from day one. Both may be required to cover rent, but the timing and documentation of their legal involvement are different.